Quick Answer, Position Sizing for Prop Firms

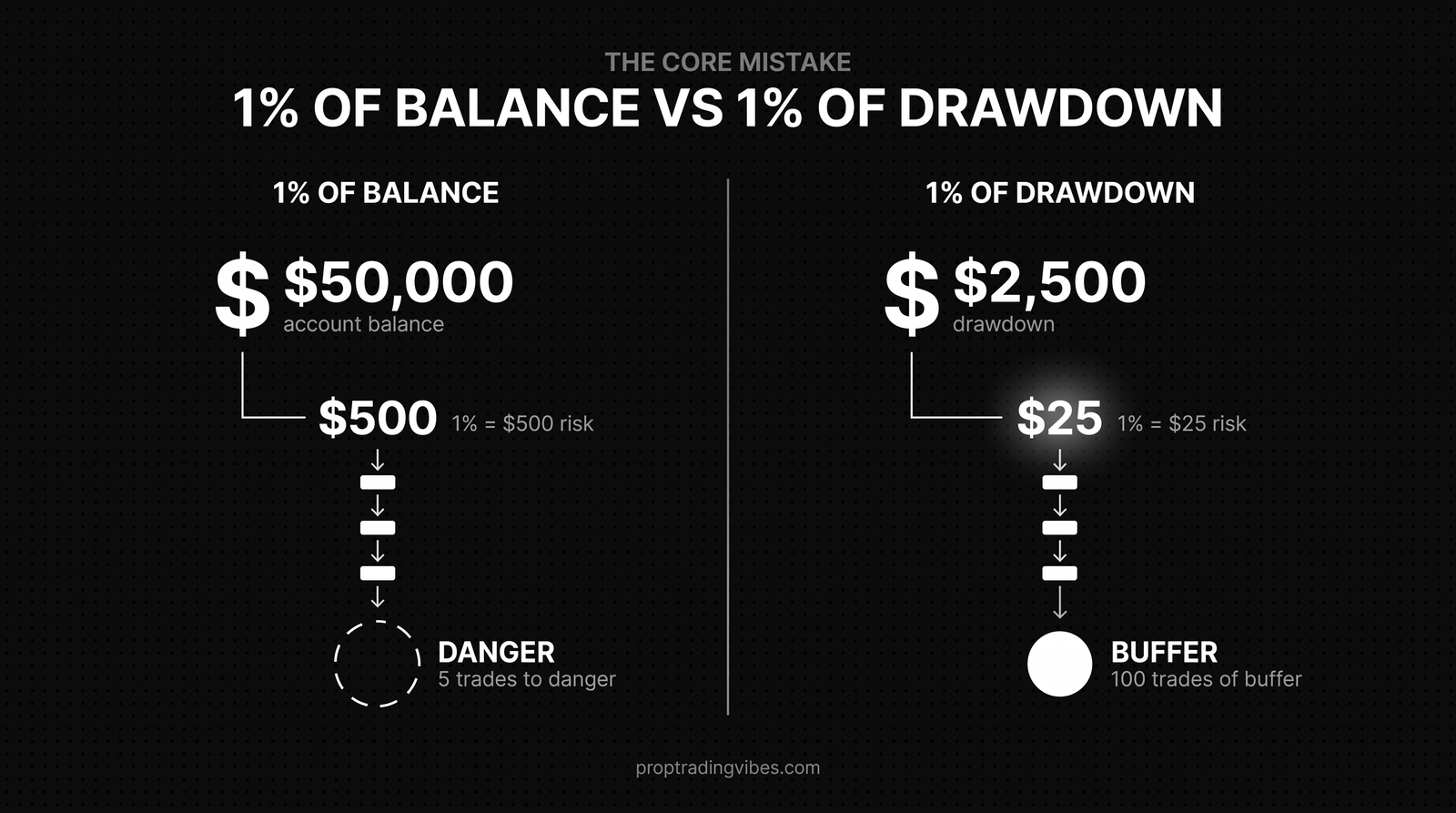

- Your risk budget is your drawdown limit, not your account balance. A $50K account with a $2,500 drawdown gives you $2,500 total to work with.

- Risk 1–2% of that drawdown per trade: $25–$50 on a $2,500 limit. Not $500 (which is 1% of the balance and will blow your account).

- Prop firms cap contract counts by account tier. Five ES on a 25K account isn't a strategy, it's a violation.

- ATR-based stops paired with drawdown risk math give you the most consistent sizing formula across products and sessions.

- Start at 30–50% of your max allocation for the first two weeks. Scale only after you've built a profit buffer.

---

Why Position Sizing Works Differently at Prop Firms

In retail trading, your position size is limited by account equity. Risk 1% of a $50K brokerage account and you're placing $500 at risk per trade. You could absorb 200 losers before the account is empty.

Prop accounts don't work that way. The $50K on the screen is buying power. Your actual risk budget is the drawdown limit, typically $2,000–$3,000 on a 50K eval. Four losing trades at $500 risk each and you've consumed 80% of that limit. The account is effectively dead.

The standard retail rule of "risk 1% of your account" becomes dangerous here. One percent of $50,000 is $500. One percent of your $2,500 drawdown is $25. Those numbers are not interchangeable.

This is the one shift that separates traders who keep funded accounts from traders who stay stuck in the eval cycle.

---

Calculating Risk Per Trade

The formula is simple:

Risk per trade = Drawdown limit × Risk percentage

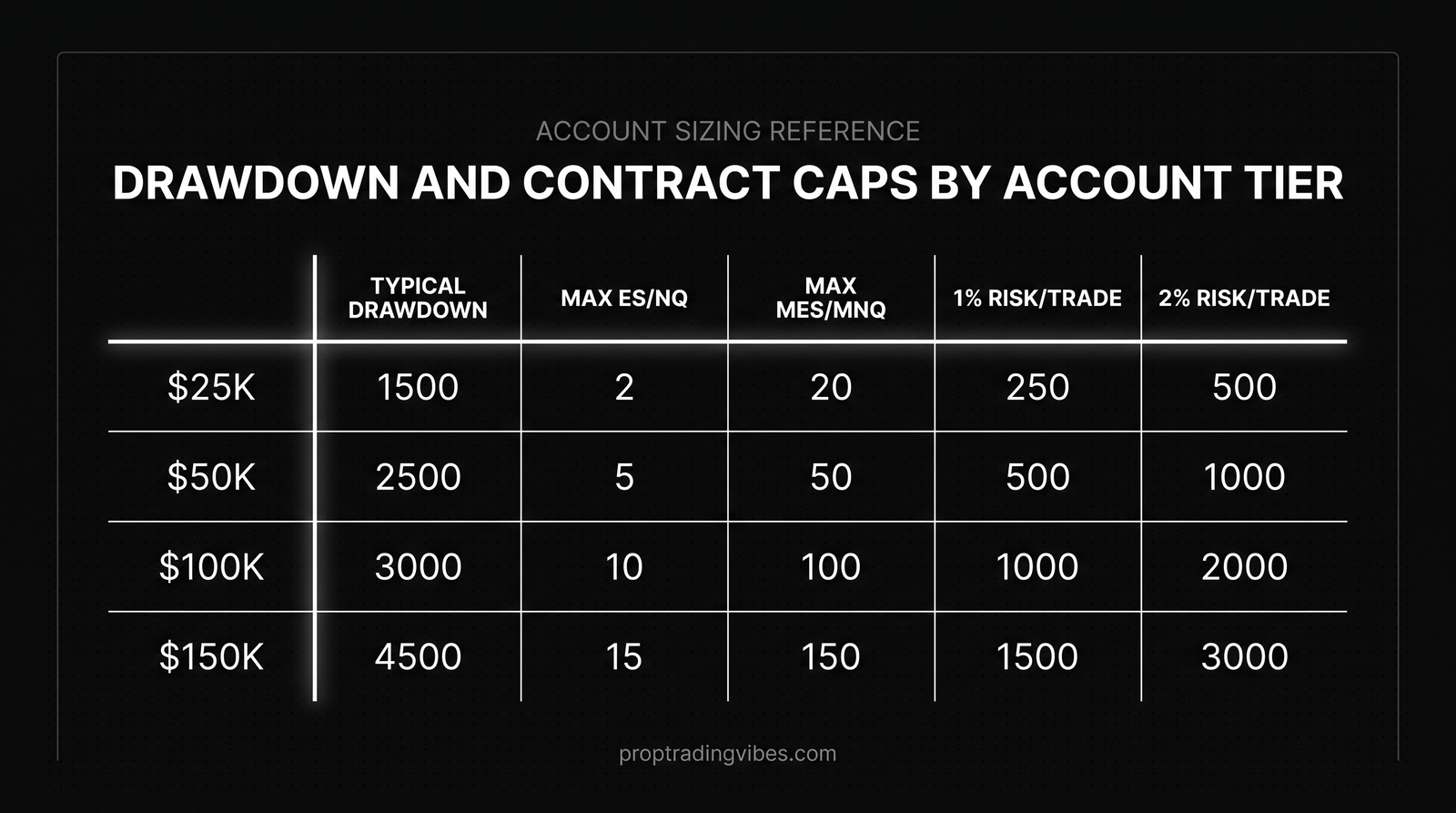

| Account Size | Typical Drawdown | 1% Risk | 2% Risk |

|---|---|---|---|

| $25K | $1,500 | $15/trade | $30/trade |

| $50K | $2,500 | $25/trade | $50/trade |

| $100K | $4,000 | $40/trade | $80/trade |

| $150K | $5,500 | $55/trade | $110/trade |

At 1% risk, a $2,500 drawdown gives you 100 losing trades before you're out. At 40% win rate (very poor) with a 1.5:1 reward, you'd still need an extraordinary losing streak to blow the account. That cushion is the point.

Daily Loss Limits Add Another Constraint

Most prop firms layer a daily loss limit on top of the overall drawdown: typically $500–$1,500 on a 50K account. Your per-trade size has to respect both.

If your daily limit is $1,000 and you're risking $400 per trade, two losers end your day, and a third could breach the limit and terminate the account. Size so you can absorb 3–4 full losers within the daily max.

More on managing drawdown thresholds

---

Contract Limits by Account Size

Every prop firm publishes maximum contract counts per account tier. These are firm rules, not suggestions.

| Account | Drawdown | Max ES/NQ | Max MES/MNQ | Max GC/MGC |

|---|---|---|---|---|

| $25K | $1,500 | 2–3 | 15–25 | 2–3 |

| $50K | $2,500 | 5–10 | 25–50 | 5–6 |

| $100K | $4,000 | 10–15 | 50–75 | 8–10 |

| $150K | $5,500 | 15–20 | 75–100 | 10–15 |

These vary by firm. Apex Trader Funding tends to be more generous with contract limits. Tradeify and TradeDay run tighter on smaller accounts. MyFundedFutures and Lucid Trading both publish specific per-product limits in their rule sets.

The contract cap is a ceiling, not a target. A 50K account that allows 10 ES contracts doesn't mean trading 10 ES is appropriate. It means the firm will let you blow up that fast if you choose to.

Understanding leverage in futures trading

---

ATR-Based Position Sizing: Step by Step

ATR (Average True Range) measures actual market movement over a defined period. It's the cleanest way to set stop distances that reflect real volatility rather than arbitrary round numbers.

The Four-Step Process

Step 1: Set your risk budget.

50K account, $2,500 drawdown, 1.5% risk = $37.50 per trade.

Step 2: Pull the ATR.

14-period ATR on a 5-minute ES chart. Say it reads 3.5 points. Multiply by 1.5 for stop distance: 3.5 × 1.5 = 5.25 points, rounded to 5.

Step 3: Calculate dollar risk per contract.

ES moves $12.50 per tick (0.25 points), so 1 point = $50. A 5-point stop on 1 ES = $250 risk per contract.

Step 4: Divide risk budget by risk per contract.

$37.50 ÷ $250 = 0.15 contracts. You can't trade fractional ES, so you use 1 MES instead ($25 risk on a 5-point stop).

Product Risk Comparison Table

| Product | Tick Value | Point Value | Typical ATR Stop | Risk/Contract | Contracts at $50 Risk |

|---|---|---|---|---|---|

| ES | $12.50 | $50 | 4–6 pts | $200–$300 | 0 (use MES) |

| MES | $1.25 | $5 | 4–6 pts | $20–$30 | 1–2 |

| NQ | $5.00 | $20 | 15–25 pts | $300–$500 | 0 (use MNQ) |

| MNQ | $0.50 | $2 | 15–25 pts | $30–$50 | 1 |

| GC | $10.00 | $100 | 3–5 pts | $300–$500 | 0 (use MGC) |

| MGC | $1.00 | $10 | 3–5 pts | $30–$50 | 1 |

On accounts with tight drawdowns (25K and 50K), micro contracts are the tool. Full-size contracts become practical at 100K+ where the drawdown gives you more margin per trade.

Risk-reward ratio explained for futures traders

---

Worked Examples by Account Size

25K Account: Trading MNQ

Drawdown: $1,500. Daily limit: $500. Risk at 1%: $15 per trade.

MNQ point value: $2. ATR stop of 20 points = $40 per contract. $15 budget doesn't cover one contract at that stop.

Options: tighten to a 7-point stop ($14 risk) or bump to $40 risk (2.6% of drawdown). Most traders accept the higher percentage on 25K accounts because there's no practical alternative. One MNQ with a real stop is already the minimum viable trade.

Treat 25K accounts as reps, not income. The drawdown is too tight for consistent income extraction.

50K Account: Trading MES

Drawdown: $2,500. Daily limit: $1,000. Risk at 1.5%: $37.50 per trade.

MES point value: $5. ATR stop of 5 points = $25 per MES. $37.50 ÷ $25 = 1.5 contracts, so 1 MES standard, 2 MES on a high-conviction setup with $500+ buffer.

Daily limit of $1,000 allows 40 MES stops. Not a binding constraint at this account size.

100K Account: Trading ES

Drawdown: $4,000. Daily limit: $2,000. Risk at 1.5%: $60 per trade.

ES stop of 4 points = $200 per contract. $60 ÷ $200 = 0.3 contracts. Even at 100K, standard ES sizing at 1.5% drawdown risk means using micros.

To trade 1 ES responsibly, you need either a $1,500+ buffer (making the effective risk 5% of starting drawdown acceptable) or a tighter stop of 1–2 points. On FOMC or CPI days when ATR doubles, the math gets even tighter.

Core risk management frameworks for prop trading

---

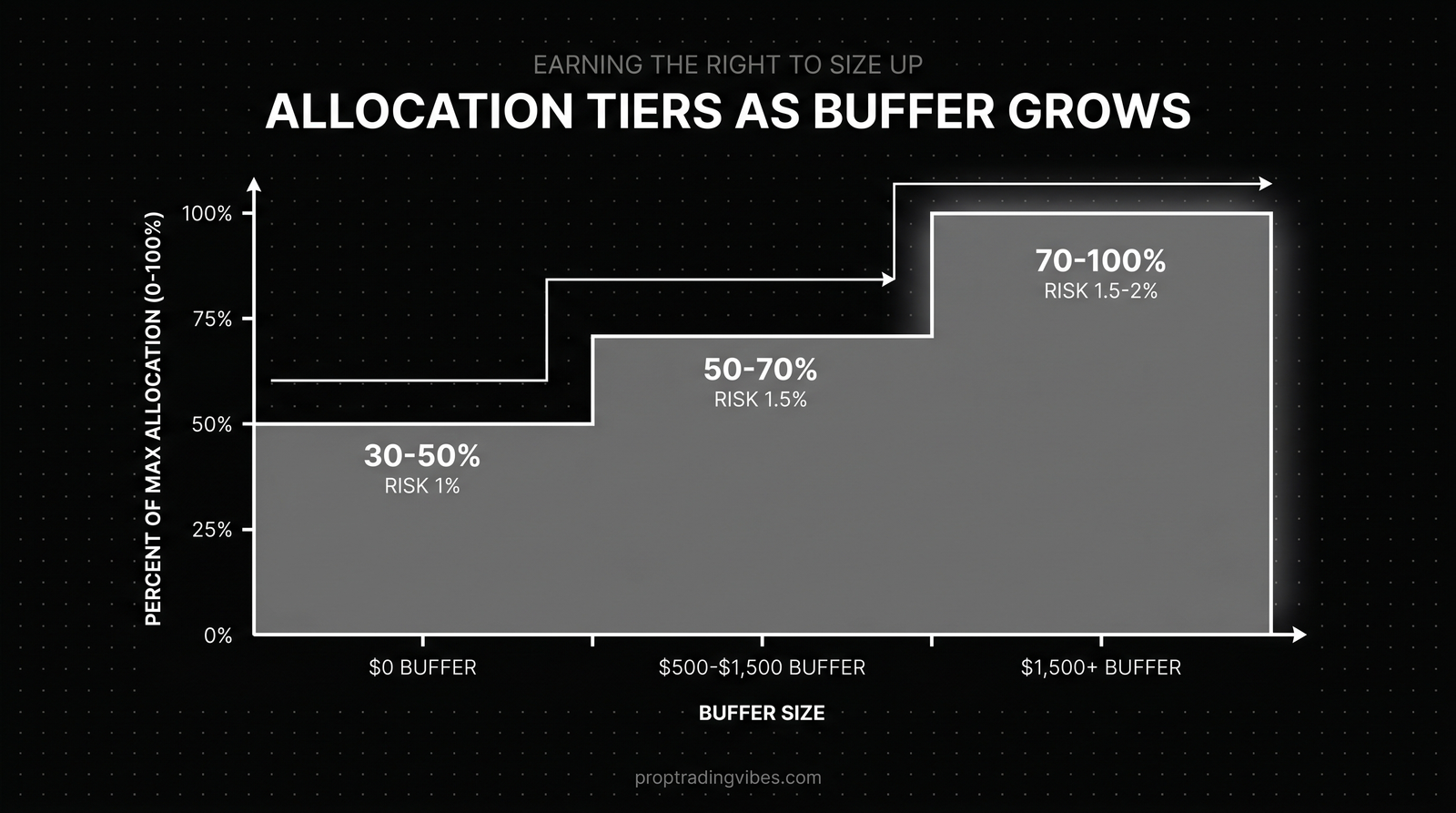

Scaling Position Size as Your Buffer Grows

Your buffer is the distance between your current balance and your drawdown floor. As the buffer grows, you earn the right to size up.

Scaling Tiers

| Buffer Level | Allocation | Risk % of Drawdown |

|---|---|---|

| $0 (day 1) | 30–50% of max | 1% |

| $500–$1,500 | 50–70% of max | 1.5% |

| $1,500+ | 70–100% of max (A+ setups) | 1.5–2% |

A few hard rules:

- Never size up after a losing day. Buffer growth earns more contracts. Losing days do not.

- Scale after a string of consistent days, not as a way to recover losses.

- On any day your available drawdown drops below $1,000, drop back to minimum size until the buffer rebuilds.

Firms like Lucid Trading and Top One Futures have EOD Trailing drawdown mechanics where the floor locks up at end of day once you're above threshold. Know whether your firm uses EOD Trailing, Intraday Trailing, or Static drawdown before you calculate your buffer.

What is trailing drawdown and how does it work

---

The Most Common Sizing Mistakes

Trading Full Contracts on Day One

Your 50K account allows 10 ES. You trade 3 on your first setup. Stop gets hit. You've burned $600 of a $2,500 drawdown on a single trade. The account is now trading scared with 76% of its room consumed.

Ignoring the Daily Loss Limit

You've lost $600. Daily limit is $1,000. You take another trade at normal size. It loses. One more similar loss and you're terminated for the day, possibly permanently depending on the firm's rules. Daily limits are hard stops, not soft guidelines at places like TradeDay and Bulenox.

Fixed Size Regardless of Volatility

Trading 2 MES on a quiet Monday and 2 MES on FOMC Wednesday are completely different risk profiles. ATR on FOMC can run 2–3x normal. Wider ATR means wider stops means fewer contracts. Adjust every session.

Sizing Up to Recover Losses

You're down $300. You double size to recover it in one trade. You lose again. Now you're down $900 and the spiral is real. This is the single fastest way to turn a recoverable day into a terminated account.

Not Accounting for Slippage and Commissions

Your calculated risk is $25 per trade. Add round-trip commissions of $3–$5 per contract plus stop-market slippage on fast moves and actual risk lands at $30–$35. On tight drawdowns, those dollars matter.

Using trailing stop losses without getting stopped out unnecessarily

---

Multi-Account Sizing Rules

Running multiple funded accounts via trade copier or manual execution requires treating each account as a separate entity.

Account A has its own drawdown. Account B has its own drawdown. They don't share risk budgets. Don't aggregate P&L across accounts and use that number to make sizing decisions on any individual account.

Where traders go wrong: they're up $500 on one account and down $300 on another. They net it out and feel fine. Then they size up on the losing account to "catch up," which now risks that account's drawdown based on a mental shortcut that has no structural basis.

The rule: identical setups get identical contract sizes on all accounts. The only variable is when one account has a larger buffer. You might trade 2 MES on a funded account with a $1,000 buffer and 1 MES on a freshly funded account with no buffer.

---

Fixed Risk vs. Percentage-Based Risk

Both work. Here's when to use each.

Fixed risk means risking the same dollar amount every trade ($30 per trade, always). Simple. Consistent. Removes daily recalculation. Works well for traders in their first few funded accounts who need mechanical discipline over flexibility.

Downside: as your buffer grows, fixed risk undersizes your opportunity. As your available drawdown shrinks after losses, fixed risk oversizes relative to remaining cushion.

Percentage-based risk recalculates daily or weekly against current available drawdown. If available drawdown is $2,500, risk $37.50. If it shrinks to $1,800, risk $27. If it grows to $3,200, risk $48.

Start with fixed risk for your first full month on a funded account. Once you're tracking your spreadsheet daily and have consistent execution, move to percentage-based.

Full risk management system for active prop traders

---

Building a Position Sizing Spreadsheet

Five minutes at the start of each week. Track these columns:

| Column | What to Track |

|---|---|

| Account + Firm | Name and current tier |

| Starting Balance | The number when funded |

| Current Balance | Updated daily |

| Drawdown Floor | Current trailing or static floor |

| Available Drawdown | Current balance minus floor |

| Daily Loss Limit | From firm rules |

| Max Risk/Trade | 1.5% of available drawdown |

| Product | MES, MNQ, MGC, etc. |

| Current ATR | Pull before session |

| Stop Distance | 1.5× ATR |

| Max Contracts | Risk/trade ÷ stop value |

Update balance and drawdown floor after each session. The spreadsheet removes sizing decisions from the trading session itself. You calculated your number before the market opened. You trade it.

---

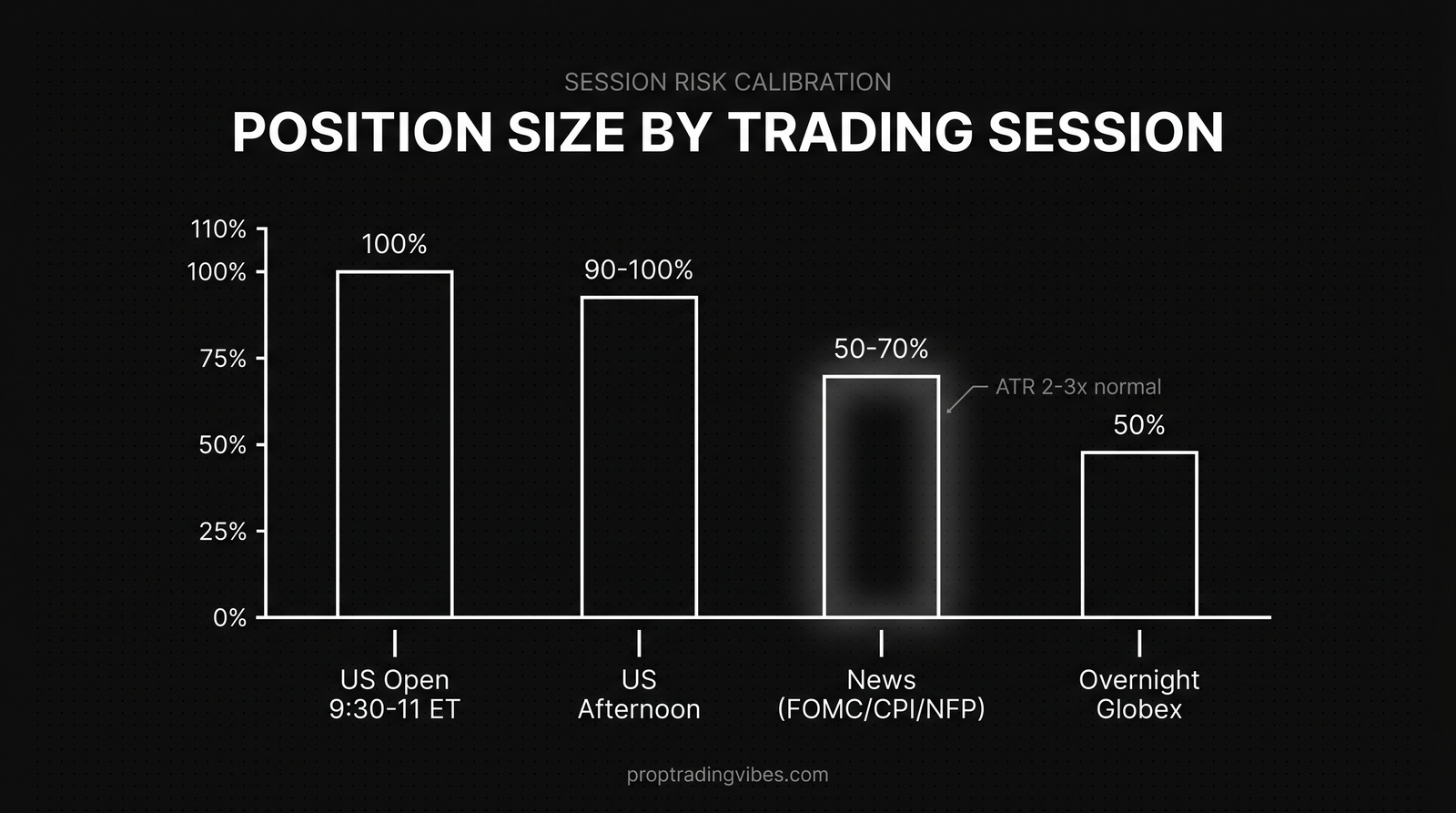

Session-Based Sizing Adjustments

Volatility varies by session. Sizing should reflect that.

| Session | Typical ATR Behavior | Size Adjustment |

|---|---|---|

| US Open (9:30–11:00 ET) | High | Standard calculated size |

| US Afternoon | Lower | Standard or –10% |

| News Events (FOMC, CPI, NFP) | 2–3x normal | Reduce 30–50% or skip |

| Overnight (Globex) | Lower liquidity, wider spreads | Reduce 50% or skip |

The accounts lost most often blow up during news events when a trader keeps their standard size while the market is printing 3x normal ATR. A 4-point stop on ES becomes a 4-point entry against a 12-point candle.

---

Frequently Asked Questions

What is the best position size for a prop firm account?

Risk 1–2% of your drawdown limit per trade. On a $50K account with a $2,500 drawdown, that's $25–$50 per trade. This gives you 50–100 trades of buffer at a 100% loss rate, which covers even extended rough stretches. Start at 1% and move to 1.5–2% only after building a profit buffer.

How many contracts should I trade on a 50K prop firm account?

Start with 1–2 MES or 1 MNQ. Full-size ES contracts typically require $200–$300 risk at normal ATR stops, which exceeds safe drawdown risk at 50K. Scale to 2–4 MES only after you have $500+ in profit buffer above your starting balance.

Should I use the same position size on every trade?

For the first 30 days on a funded account, yes. Fixed size builds consistency and removes one variable from your decision-making. After that, adjusting by setup quality (full size on A+ setups, half size on B setups) and current ATR is a reasonable progression.

How do I calculate position size using ATR?

Multiply the 14-period ATR by 1.5 to get your stop distance. Multiply that by the point value to get dollar risk per contract. Divide your trade risk budget (1–2% of drawdown) by that number to get contract count. If the result is less than 1, use micro contracts.

What happens if I trade too large on a prop firm account?

A few oversized losing trades will breach your maximum drawdown or daily loss limit. At most firms, including Apex Trader Funding, TradeDay, and Breakout, breaching either limit terminates the funded account with no second chance. The evaluation fee is gone and you restart from the beginning.

How do contract limits work at prop trading firms?

Firms cap the maximum simultaneous open contracts per account tier. A 50K account typically allows 5–10 ES or 25–50 MES as of 2026. Limits apply to total open positions. Some firms use aggregate limits across all products; others cap each product separately. Check the rules dashboard for your specific firm before your first trade.

Should I trade micros or full-size contracts on a prop firm account?

Micro contracts (MES, MNQ, MGC) are the right tool for accounts under $100K. They allow precise sizing that matches tight drawdown limits without forcing you to either skip trades or accept outsized risk. Full-size contracts make sense at $100K+ where drawdowns of $4,000–$6,000 provide enough room per trade.

What position size should beginners use on their first funded account?

Trade the minimum: one micro contract for the first 5–10 sessions regardless of what the math says. Build familiarity with the platform, the firm's order entry, and your own execution habits before putting real risk behind your trades. Scale to calculated sizes only after consistent execution at minimum size.

How does position sizing differ between evaluation and funded stages?

It shouldn't. Traders who size up during evals (because it's not real money) and then revert to smaller sizes on funded accounts fail because the funded account behavior feels unfamiliar. Trade the eval exactly as you plan to trade the funded account. The eval is a proof-of-concept, not a stress test.

Does position sizing change on high-volatility news days?

Yes, significantly. On FOMC, CPI, and NFP dates, ATR can run 2–3x its normal level. Wider ATR means wider stops means fewer contracts to stay within your drawdown risk budget. Reduce size by 30–50% on known news days or avoid trading within 30 minutes of the release entirely.