Quick Answer, Opening Range Breakout

- The opening range breakout (ORB) marks the high and low of a fixed window after the cash open, then trades the break above or below that range.

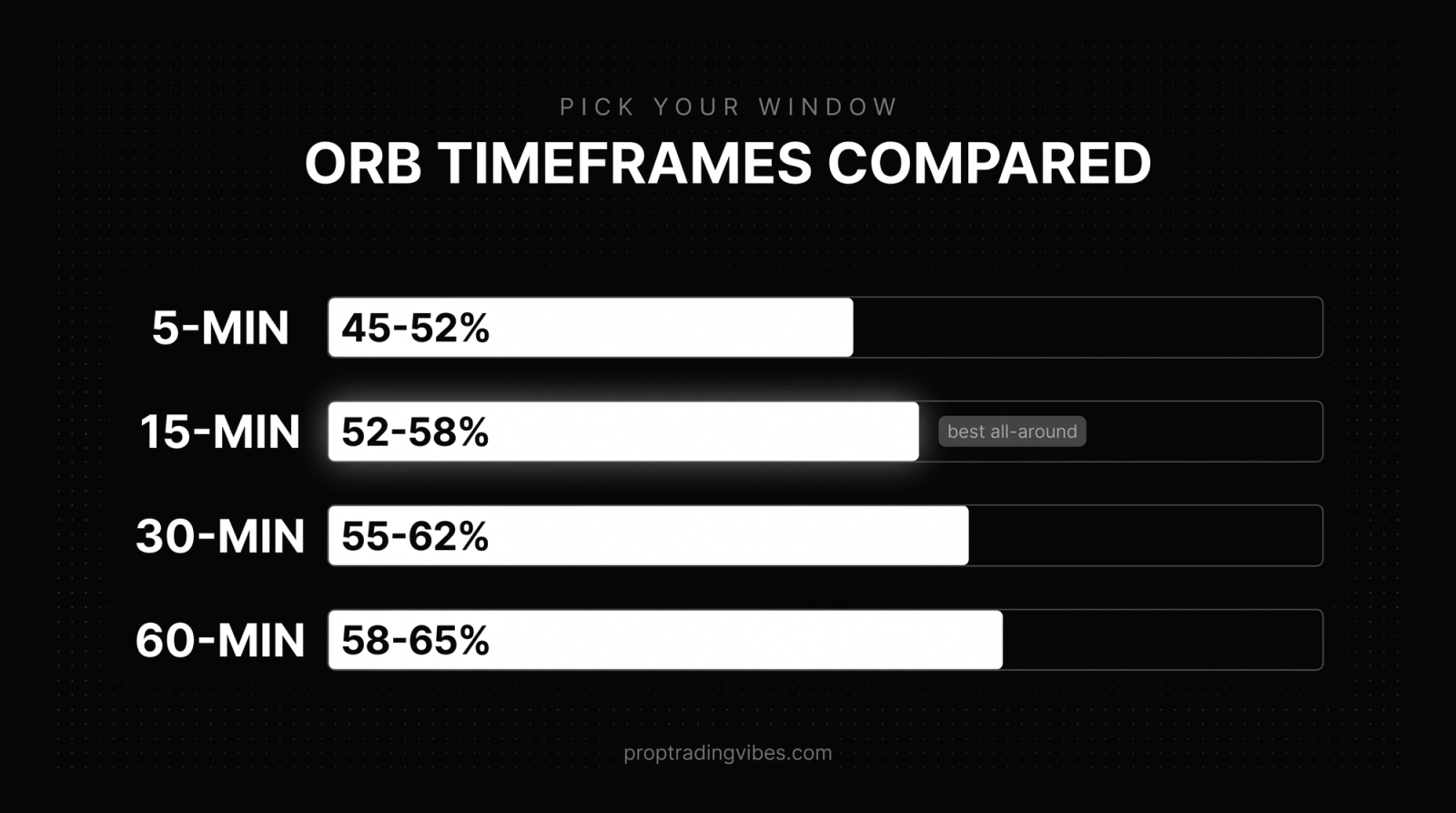

- The four common windows are 5, 15, 30, and 60 minutes from the 9:30 AM ET open, each trades signal quality against opportunity.

- The 15-minute ORB on NQ has the best balance of win rate and frequency in my logs: a clean setup roughly 3 of 5 days.

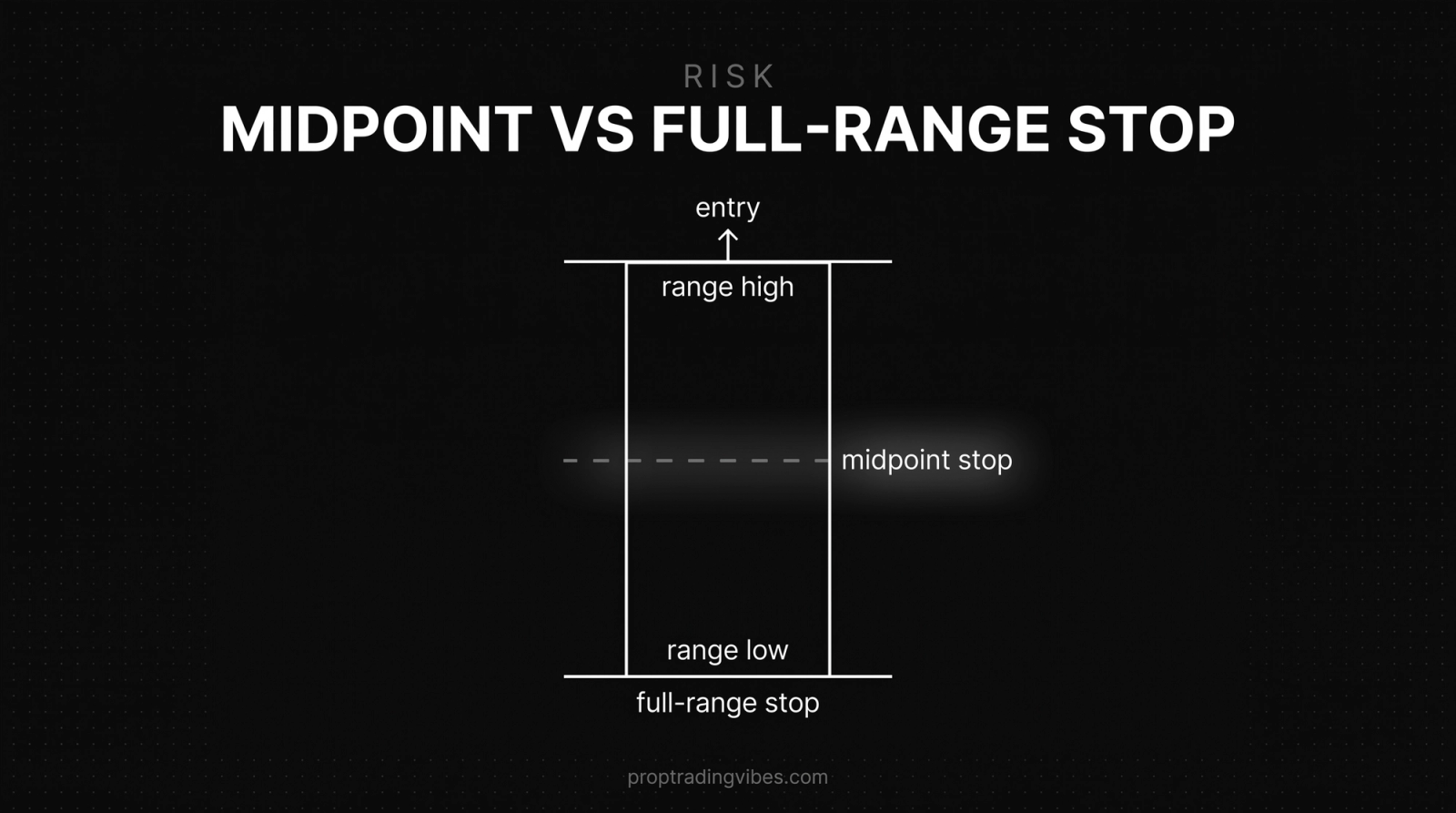

- Your stop belongs at the opposite side of the range or its midpoint, pre-defined risk that keeps you inside prop firm drawdown limits.

- The fastest way to blow an ORB account: taking breakouts on narrow-range days or ahead of FOMC, CPI, and NFP, where false breakouts run hard.

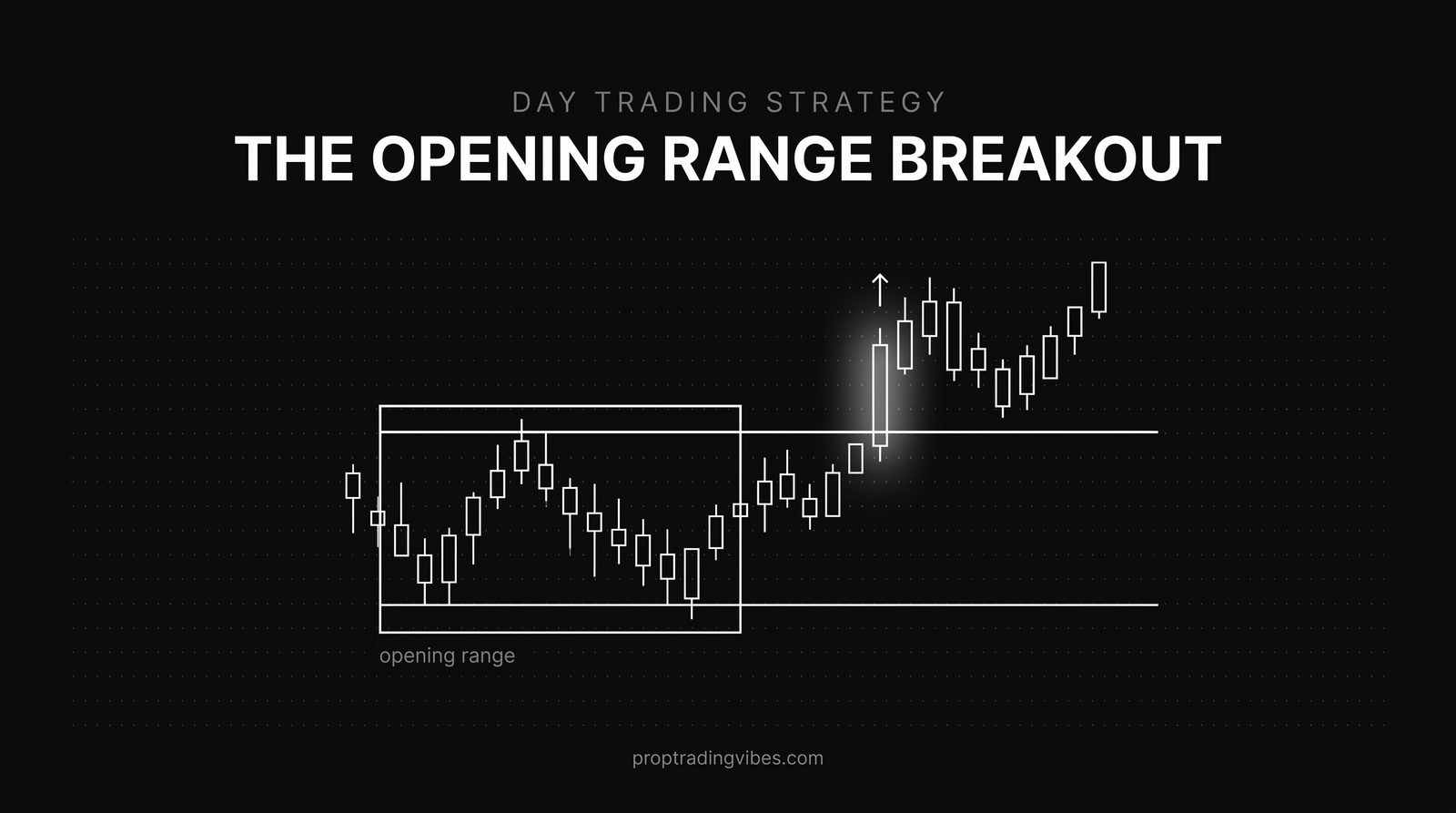

What Is the Opening Range Breakout?

The opening range breakout is a day trading strategy built on one idea: the first X minutes after the open establish a price range, and when price breaks beyond that range, it tends to continue in that direction. The "X" is your choice, five minutes, fifteen, thirty, sixty. Each gives you a different trade.

I've traded a version of ORB on NQ futures since mid-2024. It isn't the only thing I trade, but it produces the cleanest, most mechanical setups in my week. The defined risk is why it fits funded accounts so well: one blown stop can end an evaluation, and ORB hands you the stop level before you ever click buy.

This guide covers the whole strategy, what the opening range is, how to draw it, which timeframe to use, entries and stops, targets, when ORB fails, the real win rates, and the modified version I trade on NQ daily.

What Is the Opening Range?

The opening range is the high and low established during a set window after the cash market opens. For NQ (Nasdaq 100 E-mini) and ES (S&P 500 E-mini), the cash session starts at 9:30 AM Eastern. A 15-minute opening range runs 9:30 to 9:45 AM, mark the highest and lowest price in that window, and that's your range.

The concept traces to Toby Crabel's research in the late 1980s. He showed that when price broke out of a *narrow* opening range, the move that followed was larger and more reliable than breakouts from wide ranges. That insight still holds.

It works because the opening range captures the first real auction after fresh overnight information gets priced in. Institutional order flow is heaviest in the first 30 minutes of the cash session. When price breaks out of that contested zone, one side has usually won the early fight, and momentum carries.

One nuance: futures trade nearly 24 hours, so NQ has been moving since 6:00 PM the prior evening. But the cash open at 9:30 AM is where the volume and predictive value live. Overnight data supplements your read; the ORB itself keys off the cash open.

Which ORB Timeframe Should You Use?

There's no single correct window, each gives a different trade profile. Here's how the four main timeframes compare across the hundreds of NQ and ES sessions I've tracked.

| Timeframe | Avg. Win Rate | Best Markets | Typical Stop (NQ) | Notes |

|---|---|---|---|---|

| 5-Minute | 45–52% | NQ, high-beta stocks | 15–30 pts | Highest frequency, lowest win rate. Tight stops, fast resolution, big R when it works. |

| 15-Minute | 52–58% | NQ, ES, CL | 25–50 pts | Best all-around. Enough data to filter noise, still early enough for a full move. |

| 30-Minute | 55–62% | ES, NQ, YM | 40–80 pts | Higher win rate, wider stops. Misses early explosive moves. |

| 60-Minute | 58–65% | ES, bonds, FX futures | 60–120 pts | Highest win rate, widest stops, fewest setups. |

The 15-minute ORB is what I trade most on NQ. Fifteen minutes is long enough for the opening auction to settle and the real direction to emerge, but early enough to catch a full-session move. The NQ 15-minute range averages 30–45 points on a normal day, a comfortable full-range stop on a $50K account.

The 30-minute is the classic Crabel window and the most reliable signal, but by 10:00 AM a chunk of the day's range is already spent. I use it more on ES, which is slower and more institutional. The 60-minute has the best win rate in my logs and I rarely trade it: the stop is so wide that sizing on an evaluation account gets restrictive.

How to Draw the Opening Range Correctly

- Set your chart to the cash open, 9:30:00 AM ET on NQ and ES. Not 9:29, not the overnight session.

- At the end of your window, mark the high and the low. I use wicks, not bodies, I want the full range including rejection. The difference tests out marginal either way.

- Extend both lines forward through the session. Above the high is a long trigger; below the low is a short trigger.

- Mark the midpoint. It's my stop level on most trades and a momentum reference: if price breaks out then sags back to the midpoint, the breakout is weakening.

Sierra Chart has a native Opening Range study; NinjaTrader and TradingView both have ORB scripts. The mistake I see most: traders measure from the wrong session start. If your feed opens the session at 6:00 PM ET, "the first 15 minutes" is 6:00–6:15 PM, not the opening range. Platform settings matter.

Entry Rules: Filtering False Breakouts

Trade ORB purely mechanically and false breakouts will grind you down. My refined rules for the 15-minute NQ ORB:

- Wait for a close beyond the level. I don't enter on the tick that touches the high, I wait for a 5-minute candle to close past it with commitment. A wick poke that reverses is not a breakout.

- Demand volume. A real breakout attracts participation. If price drifts through the level on declining volume, I pass.

- Check overnight context. A breakout into open air (above the overnight high) beats a breakout into the middle of the overnight range, which is often just noise.

- Skip the first false breakout. On NQ the *first* break of the range is a trap more than 40% of the time. I let it happen; if price re-enters the range and breaks out again in the same direction, that second break, the "retest and go", is far more reliable.

- Skip narrow ranges. Under 20 points on the NQ 15-minute window, I don't trade. No real auction, no edge.

This sits inside the broader breakout trading playbook, confirmation and the retest are what separate a tradable breakout from a liquidity grab.

Where to Place Your Stop

Two schools, both tested over 200+ trades.

Full-range stop: long above the range high, stop below the range low. Maximum room, but your risk is the entire range width, 40+ points on a normal NQ day.

Midpoint stop: stop at the center of the range. Cuts risk in half. The logic: if price breaks out then falls all the way back to the midpoint, the breakout has already failed, you don't need it to travel to the far side to know you're wrong.

I use the midpoint stop. It gets stopped out more often, but the winners deliver a much better R-multiple because initial risk is smaller relative to target. On a 40-point NQ range, the midpoint stop sits ~20 points from entry; a 60-point run is then 3:1 instead of 1.5:1. The one exception is very tight ranges (20–25 points), where the midpoint would sit inside the noise, there I use the full-range stop.

Setting Targets

Targets key off the range width itself:

- 1x extension (project the range height from the breakout level), hits on ~60–65% of valid breakouts.

- 1.5x extension, ~45–50%. I take partials at 1x and trail to 1.5x.

- 2x extension, the runner, frequent on trend days, ambitious on normal ones.

I scale out: enter with 3 NQ micros, take one off at 1x, one at 1.5x, and trail the last with the stop at breakeven after the first target. With a 20-point stop and a 40-point first target, that's 2:1 on the first scale, meaning I only need to win ~34% to break even, and filtered second-breakout entries win closer to 55%. The math runs in your favor.

Combining ORB with Gap Analysis

Layering gap analysis onto ORB is the single most impactful filter I've added.

- Gap up + break above the range = strong long. Buyers in control, vacuum below, momentum with you. My highest-probability setup.

- Gap up + break below the range = gap-fill short, targeting the prior close. NQ gap fills complete ~70% of the time when the break below happens in the first 45 minutes.

- Gap down + break below = strong short (mirror image).

- Gap down + break above = reversal, the trickiest; big when it works, fails more often, so tighter stops and smaller size.

Gap size matters: I filter out ORB entirely when the NQ gap is under ~10 points. Small gaps produce indecisive ranges. At 30+ points, the range usually forms with clear bias.

What's the ORB Success Rate?

There's no single honest number, it depends on timeframe, market, and how hard you filter. The table above is the realistic spread: 45–52% on the 5-minute up to 58–65% on the 60-minute, *before* filters.

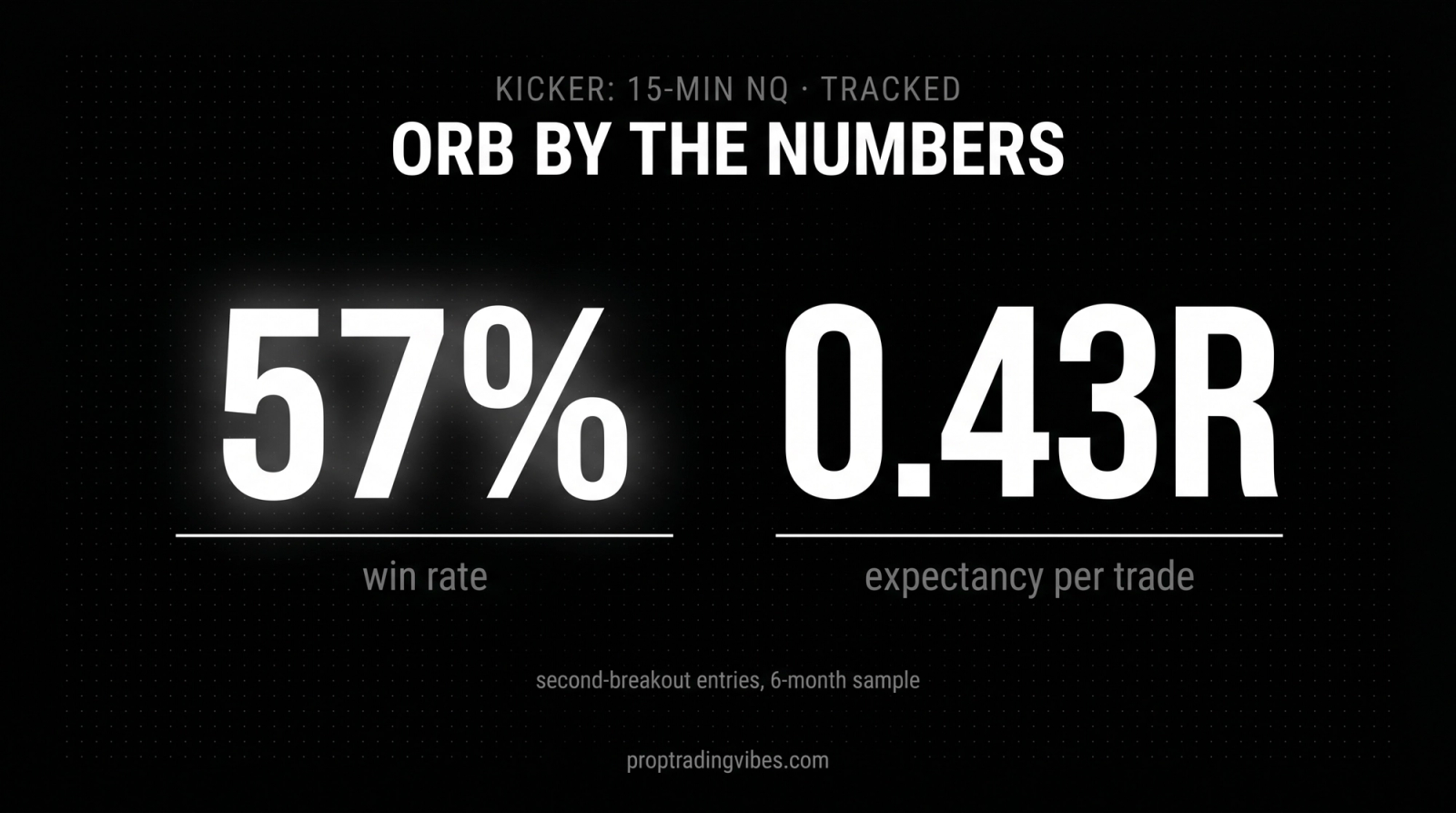

What actually matters is expectancy, not raw win rate. As of June 2026, my tracked 15-minute NQ stats on second-breakout entries over the prior six months: 57% win rate, average winner 1.8R, average loser 1.0R, a positive expectancy of roughly 0.43R per trade. Nothing spectacular. Consistent enough to pass evaluations and stay funded, which is the entire job.

Anyone quoting a precise "ORB win rate" without naming the timeframe, the market, and the filters is selling you something. Build your own number, see the backtesting section below.

Why ORB Works for Prop Firm Evaluations

- Defined risk before entry. You know your stop in points before you trade, so you can size to stay inside the firm's drawdown. No "I'll move it if it goes further."

- Quick resolution. Most ORB trades resolve within 60–90 minutes. You're not holding all day hoping.

- Objective rules kill emotion. Two losing days into an evaluation, mechanical rules are what save the account. The levels are the levels.

- One trade per day is often enough. ORB gives one, maybe two setups a day, that forces the discipline overtrading destroys. It also makes the strategy trivial to journal and review.

If you're still choosing where to run it, our guides to the best prop firms for day trading and the rules every funded account enforces pair directly with this setup.

When to Skip an ORB Setup

- High-impact news days, FOMC, CPI, NFP. On CPI days the 8:30 AM move often exhausts the day's range before the cash open. I skip ORB entirely and only consider a separate post-announcement setup. (More in trading during news events.)

- Narrow opening ranges, under 20 points on NQ means indecision; breakouts fail at a much higher rate.

- Range-bound overnight, no overnight trend, no gap, no catalyst, and the day is likely a chop. That's a range day, not a breakout day.

- Monday mornings, anecdotally my worst ORB results; institutional volume eases into the week.

- Triple-witching / expiration weeks, hedging flows distort the range. Reduce size or skip.

My Modified NQ ORB

My version isn't textbook. I trade the 15-minute NQ range but never the first breakout, I wait for it to fail or succeed, then trade the *second* move once the weak hands are shaken out. Entry on the second break above the high, stop at the midpoint.

I layer gap bias on top: with a 30+ point gap up and the range forming entirely above the prior close, I'm long-only that session and won't fade the gap unless it's already 80%+ filled in the first 15 minutes.

Sizing is fixed at 1% risk per trade. On a $50K account that's $500. With a 20-point midpoint stop on NQ micros ($2/point), that's 12 micros; a 30-point stop is 8 micros. The size flexes with the range, the dollar risk stays constant. After the first target hits, I take 50% off and trail the rest to the breakout level, no round trips, no giving gains back.

Fewer setups than pure ORB (2–3 a week), higher quality, shallower drawdowns. That's the whole point when you're managing several funded accounts at once, like Lucid Trading, Top One Futures, and FundingPips.

How to Backtest and Validate ORB

You can forward-test ORB with a spreadsheet before risking a cent. Each morning, mark the 15-minute range: high, low, midpoint, width. Then log whether the first breakout was true or false, where price went versus the 1x/1.5x/2x targets, and whether the day trended or chopped. After 20 sessions you'll have a win rate, an average range width, and a false-breakout frequency specific to *current* conditions, worth more than any course built on five-year-old data. The deeper method is in our guide to backtesting trading strategies.

The bottom line: ORB earns its permanent spot in my playbook because it captures the highest-conviction price action of the day and converts it into a trade with defined risk, clear targets, and fast resolution. It won't make you rich on one trade. Combined with gap filters and the discipline to skip bad setups, it produces a positive expectancy that compounds, and if you trade NQ or ES on a funded account without a structured plan for the first 15 minutes, you're leaving edge on the table.

Frequently Asked Questions

What is the opening range breakout strategy?

The opening range breakout (ORB) strategy marks the high and low of a set window after the open and trades in the direction of the break beyond that range. Traders use 5, 15, 30, or 60-minute windows from the 9:30 AM ET cash open on US index futures. It was popularized by Toby Crabel in the late 1980s and remains one of the most widely used intraday approaches.

Which ORB timeframe is best for NQ futures?

The 15-minute opening range works best on NQ for most traders. It captures enough of the initial auction to filter early noise while leaving time for a full-session move. On NQ the 15-minute range averages 30–45 points on a normal day, which gives comfortable stop placement on a funded account.

What is the success rate of the opening range breakout strategy?

It varies by timeframe and market. On NQ, the 5-minute ORB wins roughly 45–52%, the 15-minute 52–58%, the 30-minute 55–62%, and the 60-minute 58–65%, before filtering. Win rate matters less than expectancy: my filtered 15-minute second-breakout entries run ~57% at about 0.43R per trade. Filters (gap context, minimum range width, waiting for a confirmed second break) move the needle most.

Where should you place your stop on an ORB trade?

Two approaches: the opposite side of the range (maximum room, wider risk) or the midpoint (half the risk, still a logical invalidation). On a 15-minute NQ ORB the midpoint stop typically sits 15–25 points from entry and produces better risk-adjusted returns over a large sample.

How do you set profit targets for ORB trades?

Targets are multiples of the range width. The 1x extension hits ~60–65% of the time on valid breakouts, 1.5x about 45–50%, and 2x on strong trend days. A common method: take half at 1x, a quarter at 1.5x, and trail the rest toward 2x with a breakeven stop.

Does the opening range breakout work for prop firm evaluations?

Yes, it gives defined risk before entry, resolves within 60–90 minutes, and runs on objective rules that cut emotional decisions during stressful evaluations. Most evaluations reward consistent, controlled-drawdown performance, which is exactly what ORB produces.

How do you filter false breakouts on the opening range?

Wait for a candle to close beyond the level rather than entering on the first tick, confirm with a volume spike, check overnight context for bias, and, most important, let the first breakout play out and enter on the second break in the same direction. On NQ the first break is a false breakout more than 40% of the time, which is why the "retest and go" is the reliable entry.

When should you avoid trading the opening range breakout?

Skip it on FOMC, CPI, and NFP days when the pre-open move exhausts the range; when the NQ range is under 20 points; when the overnight session was range-bound with no catalyst; on Monday mornings when volume is lighter; and during triple-witching expiration weeks when hedging flows distort price.